(September 12, 2018 – Shenzhen, China) China will continue to be a major driver in the global silver market for years to come, fueled by continued industrial demand and silver mining activity. China is by far the largest consumer of silver globally, accounting for 18% of global fabrication demand in recent years. In addition, to meet its robust demand needs, the country is a major destination for imported silver products fabricated in the U.S., Japan and other countries. Moreover, China is also the third largest silver producing country worldwide and is a key nation for processing primary raw materials from around the world.

Important industrial uses, as well as investment, bullion trade, jewelry and silverware demand are examined in a new report, Prospects for the Chinese Silver Market. This publication was released today by the Silver Institute at the 17th China International Silver Conference in Shenzhen, China, at which the Silver Institute serves as a host. The report was researched and produced by Metals Focus, a leading precious metals consultancy based in London.

Highlights of the report include:

Photovoltaic Demand: China’s consumption of silver for solar applications has been rising in recent years to an estimated 65 million ounces (Moz) in 2017. More than 70 percent of global solar panel production takes place in China and local powder fabricators are only able to satisfy a portion of the essential powder and paste for manufacturing, therefore relying in imported silver to fulfil their requirements. Although policy changes will most likely see volumes decline modestly this year, the long-term uptrend is expected to resume in 2019, assisted by still sizable local installations and strong sales abroad.

Electronic and Electrical Demand: Growth across a wide range of end-use applications has and will continue to fortify demand. Significant areas of growth include touch panels, light emitting diodes (LEDs) and equipment used in electricity generation. Chinese consumption of silver for electronic and electrical uses was estimated at 78 Moz in 2017 and is forecast to grow modestly this year.

Brazing Alloys & Solder: Brazing applications that rely on silver should experience further gains in the years ahead, as China continues to focus on infrastructure development. Brazing alloys and solders accounted for 24 Moz in 2017. A wide range of end-use applications, including railway infrastructure development, increasing car sales, refrigeration and air conditioning should fuel this growth.

Brazing Alloys & Solder: Brazing applications that rely on silver should experience further gains in the years ahead, as China continues to focus on infrastructure development. Brazing alloys and solders accounted for 24 Moz in 2017. A wide range of end-use applications, including railway infrastructure development, increasing car sales, refrigeration and air conditioning should fuel this growth.

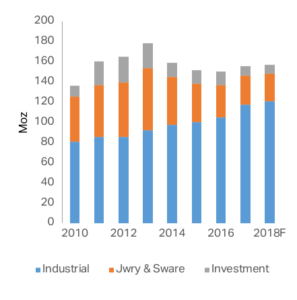

Jewelry & Silverware: Jewelry and silverware have suffered declines in China in recent years, with combined fabrication reaching 29 Moz in 2017. The main drivers of this have been changing consumer appetites and the impact of anti-corruption legislation on the gifting market. The authors, however, believe the end of this downtrend is near. In fact, silverware has already turned a corner, while silver jewelry in China is expected to return to positive growth from 2020 onwards.

Further analysis is presented in the publication, which can be downloaded for free at this link: Prospects for the Chinese Silver Market

The Silver Institute is a non-profit international industry association headquartered in Washington, D.C. Established in 1971, the Institute’s members include leading silver producers, prominent silver refiners, manufacturers and dealers. The Institute serves as the industry’s voice in increasing public understanding of the value and the many uses of silver. For more information on the Silver Institute, silver’s important uses in industry, or silver in general, please visit: www.silverinstitute.org.

Contact:

Michael DiRienzo

The Silver Institute

Tel: +1 202-495-4030

e-mail: Mdirienzo@silverinstitute.org

Nikos Kavalis

Metals Focus

Tel: +44 7734 941437

e -mail: nikos.kavalis@metalsfocus.com

Recent Comments