(Washington, D.C. – April 22, 2020) – Global silver demand was pushed higher in 2019, with a 12 percent increase in investment demand as retail and institutional investors focused their attention on the long-term investment appeal of the white metal. Favorable structural changes, such as vehicle electrification and a rebound in the key field of photovoltaics, fueled solid industrial demand.

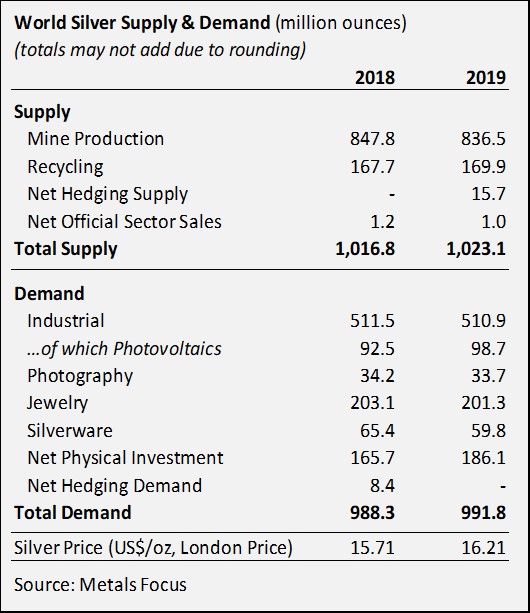

Total global silver demand in 2019 grew by 0.4 percent despite an ongoing global trade war affecting many industries. Silver industrial demand was resilient, slipping by 0.1 percent last year, with several key segments of silver industrial fabrication expanding, primarily silver’s use in photovoltaics, which grew by 7 percent to its second highest annual level. Of note, for the fourth consecutive year, silver mine supply declined in 2019, falling by 1 percent.

These developments, along with many other highlights, are discussed in World Silver Survey 2020, released today by the Silver Institute. In addition to a review of the key developments in 2019, this year’s Survey also examines the outlook for the 2020 silver market. The Survey was researched and produced for the Silver Institute by Metals Focus, the London-based independent precious metals consultancy.

Silver Investment and Price

Global silver investment jumped 12 percent to 186.1 million ounces (Moz), making it the largest annual growth since 2015. Notable gains in Europe (+25 percent), the US (+9 percent) and India (+5 percent) led to the increase. Institutional investment fared even better than retail demand. Last year, exchange-traded product (ETP) holdings stood at 728.9 Moz at year-end, up by 13%, achieving the largest annual rise since 2010.

Notably, money-managers’ net positions in Comex futures went from being short over much of 2018 to consistently positive in the second half of 2019. Coins and medals saw a 13 percent increase in demand over 2018, rising to 97.9 Moz, while bar demand remained solid at 88.2 Moz.

Combined, these were the key drivers for the 15 percent intra-year rise in the silver price to a three-year high of $19.65 last September. The 2019 yearly average silver price of US$16.21 was 3 percent higher than the 2018 average price.

Silver Demand

Global silver demand edged higher in 2019 to 991.8 Moz, up 0.4 percent, as higher net-physical investment was offset by lower jewelry and silverware demand. Industrial fabrication was nearly unchanged from 2018 at 510.9 Moz. Although the escalating trade war between China and the US weighed on industrial offtake last year, losses were broadly mitigated by favorable structural changes, such as vehicle electrification and a rebound in the key field of photovoltaics. Photovoltaic demand registered an impressive 7 percent increase in offtake, rising to its second highest annual level, while silver’s use in brazing alloys rose 1 percent.

Jewelry posted a 1 percent decrease to 201.3 Moz, primarily due to soft demand in India and China. In contrast, Thailand achieved a 13 percent increase last year and growth was also registered in Indonesia, Japan and Italy. Silverware fell by 9 percent last year almost entirely due to lower demand from India.

Silver Supply

Global mine production fell for the fourth consecutive year in 2019 by 1.3 percent to 836.5 Moz. This was a result of declining grades at several large primary silver mines and disruption-related losses at some major silver producers. Primary silver production declined by 3.8 percent in 2019 to 240 Moz. On a country basis, the largest production declines were led by Peru, followed by Mexico and Indonesia, which were partially offset by gains in Argentina, Australia and the US. Globally, Mexico was the leading silver producer last year, followed by Peru, China, Australia and Russia. Total recycling edged higher in 2019 by 1.3 percent, chiefly due to an increase in industrial and jewelry and silverware recycling.

An increase in hedging activity in the second half of 2019, at 15.7 Moz, saw the global hedge book increase for the first time since 2014. Net supply from the official sector fell last year to 1 Moz.

Outlook for 2020

The uncertainties presented by the COVID-19 pandemic make forecasting silver market conditions over the rest of the year very challenging.

With the difficulties currently facing the global economy, key areas of silver demand — including industrial fabrication and jewelry and silverware offtake — are anticipated to fall this year, solely as a result of the global pandemic.

Mine supply is expected to continue its decline given the temporary shutdown of mining operations in several significant silver mining countries in early 2020.

Silver physical investment is forecast to extend its gains this year, with a projected 16 percent rise to a five-year high as investors rotate out of equities in search of safe haven vehicles.

Additionally, Metals Focus expects silver to outperform gold later this year, which could see it test US$19.00 again before year-end.

About the World Silver Survey and Ordering Information

The Silver Institute has published this annual report on the global silver market since 1990, to bring dependable supply and demand statistics to market participants and the public. This 30th edition of World Silver Survey was independently researched and produced by Metals Focus. The report was sponsored by 18 companies and organizations from North and South America, Europe and Asia.

Copies of the World Silver Survey 2020 are available to the media upon request and a complimentary PDF version can be downloaded from the Institute’s website at www.silverinstitute.org. In North America, hard copies may be purchased by the public from the Institute’s website; for copies outside North America, please contact Metals Focus at www.metalsfocus.com.

Contact:

Michael DiRienzo

The Silver Institute

+1 202-495-4030

mdirienzo@silverinstitute.org

Philip Newman

Metals Focus

+44 203 301 6522

philip.newman@metalsfocus.com

Recent Comments