Posted on 04 17, 2024

Silver Demand for Photovoltaics Increased 64 Percent, Surpassing Estimates

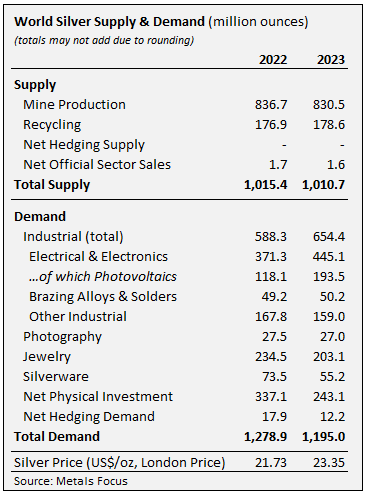

(New York City – April 17, 2024) On the heels of 2022’s record use of silver in industrial applications, a new record high was set in 2023 at 654.4 million ounces (Moz). Ongoing structural gains from green economy applications underpinned these advances as they did in 2022. Higher than expected photovoltaic (PV) capacity additions and faster adoption of new-generation solar cells raised global electrical & electronics demand by a substantial 20 percent. At the same time, other green-related applications, including power grid construction and automotive electrification, also contributed to the gains.

Overall, silver demand exceeded silver supply in 2023 for the third consecutive year, resulting in a structural market deficit of 184.3 Moz.

These and many other key aspects of the 2023 silver market are examined in World Silver Survey 2024, released today by the Silver Institute. The 88-page Survey also provides an outlook for this year’s silver market. The Survey was researched and produced for the Silver Institute by Metals Focus, the London-based independent precious metals consultancy.

Some of the key findings include:

Silver Demand

Total silver demand saw a decline of 7 percent to 1,195 Moz in 2023; however, this was coming off a record 2022. The price-sensitive physical investment, jewelry, and silverware sectors mainly contributed to last year’s drop. In sharp contrast, industrial demand hit another record high, led by the electrical and electronics sector, which grew 20 percent to 445.1 Moz last year. This gain reflects silver’s essential and growing use in PV, which recorded a new high of 193.5 Moz last year, increasing by a massive 64 percent over 2022’s figure of 118.1 Moz. Underpinning these overall gains was the limited scale of thrifting and substitution, as silver remains irreplaceable in many applications.

Chinese silver industrial demand rose by a remarkable 44 percent to 261.2 Moz, primarily due to growth for green applications, chiefly PV. Last year, China’s rapid expansion of PV production accounted for over 90 percent of global panel shipments. Industrial demand in the United States stood at 128.1 Moz, essentially flat over 2022, while Japan’s industrial offtake was also basically unchanged at 98.0 Moz.

Silver demand for ethylene oxide (EO) catalysts remained robust because of solid gains from capacity expansion. Brazing alloys rose by 2 percent due to increased mainstream end-uses, including automotive, aerospace, and shipbuilding in most major industrial countries.

Silver jewelry fabrication fell by 13 percent in 2023 to 203.1 Moz. The losses were concentrated in India, where demand eased after reaching its highest total in 2022. Excluding India, total global losses were modest at 3 percent. This was mainly due to the weakness of US and European jewelry consumption (due to such drivers as cost-of-living issues) plus destocking by retailers.

Silverware demand in 2023 fell by 25 percent to 55.2 Moz. This mainly reflected an elevated base in 2022 when fabrication achieved a record high. As with jewelry, overall losses were almost entirely due to India, owing to high local silver prices.

After five consecutive annual gains, silver physical investment (silver bar and coin demand) fell by almost a third last year to a three-year low of 243.1 Moz. While all significant markets saw losses, the decline was particularly acute in Germany (-73 percent) following the Value Added Tax increase at the start of 2023. Most other Western markets saw steep declines due to cost-of-living issues and range-bound prices. However, one partial exception was the US, where losses were smaller at 13 percent. Elsewhere, physical investment in India was down a hefty 38 percent as record high rupee silver prices led to profit-taking, while fresh investors had only limited windows for bargain hunting. The growing popularity of exchange-traded products in India also impacted physical investment in the country.

Silver Supply

Global silver mine production fell by 1 percent to 830.5 Moz in 2023. Output was significantly affected by the four-month suspension of operations at Newmont’s Peñasquito mine in Mexico following a labor strike. Mexico’s silver output fell by 5 percent to 202.2 Moz. In addition, lower ore grades and some mine closures negatively impacted production in Argentina, which experienced a 4.9 Moz drop in production, Australia at -3.1 Moz, and Russia at -1.4 Moz. However, these losses were somewhat mitigated by increased supply from Chile at +10.1 Moz and Bolivia at +3.8 Moz.

Last year, Mexico was the leading silver mining country, followed by China, Peru, Chile, and Bolivia.

Silver recycling, which accounted for 18 percent of total supply last year, grew by 1 percent to 178.6Moz. Much like 2022, the industrial sector was the primary driver of volumes, which in turn was due to growth in the recycling of EO catalysts.

This year is expected to be a solid year for total silver demand, which is forecast to grow by 2 percent. Industrial fabrication should post another all-time high, rising by 9 percent, propelled by an anticipated 20 percent gain in the PV market and healthy offtake from other industrial segments. Jewelry and silverware fabrication are predicted to rise by 4 and 7 percent, respectively, while bar & coin demand is forecast to contract by 13 percent.

Outlook for Silver in 2024

Total silver supply should decrease modestly by 1 percent. As a result, this year, we will also see another large deficit for silver, amounting to a projected 215.3 Moz, the second-largest market deficit in more than 20 years.

As outlined in the Survey, silver has many exciting new demand opportunities beyond its traditional applications and expanding role in the energy transition. For example, silver will become an indispensable material as artificial intelligence (AI) rises. End uses expected to incorporate silver in AI include transportation, nanotechnology, biotechnology, healthcare, consumer wearables, computing, and energy in data centers.

Silver Price

The average silver price grew by 7 percent in 2023, and as of April 12 this year, the silver price has increased 30 percent since the beginning of this year. As a result, the gold:silver ratio fell below 82:1, its lowest since early December 2023.

About the World Silver Survey and Ordering Information

The Silver Institute has published this annual report on the global silver market since 1990 to bring reliable supply and demand statistics to market participants and the public. Metals Focus independently researched and produced the 34th edition of World Silver Survey. The report was sponsored by 24 companies from North and South America, Europe, and Oceania.

A complimentary PDF version of World Silver Survey 2024 can be downloaded from the Institute’s website at www.silverinstitute.org. In North America, hard copies may be purchased from the Institute’s website; for copies outside North America, please contact Metals Focus at www.metalsfocus.com. In addition, members of the media and government officials can request complimentary hard copies of the Survey directly from the Silver Institute.

Contacts:

Michael DiRienzo

Silver Institute

+1 202-495-4030

mdirienzo@silverinstitute.org

Philip Newman

Metals Focus

+44-203-301-6522

philip.newman@metalsfocus.com

Recent Comments